The right loan for nursing school students

With our undergraduate loan, you can get the money you need for nursing school and pursue your passion.

3.49%

to 15.99% APRfootnote 1

What are fixed rates?

Fixed means your interest rate never changes.

If you want a predictable monthly payment, this is the way to go.

4.54%

to 14.71% APRfootnote 1

What are variable rates?

Variable interest rates go up or down as the market changes.

This means your monthly payments may also change—they might be higher if interest rates rise and lower if they fall.

Loan benefits you won't want to miss

Breaking down your repayment options

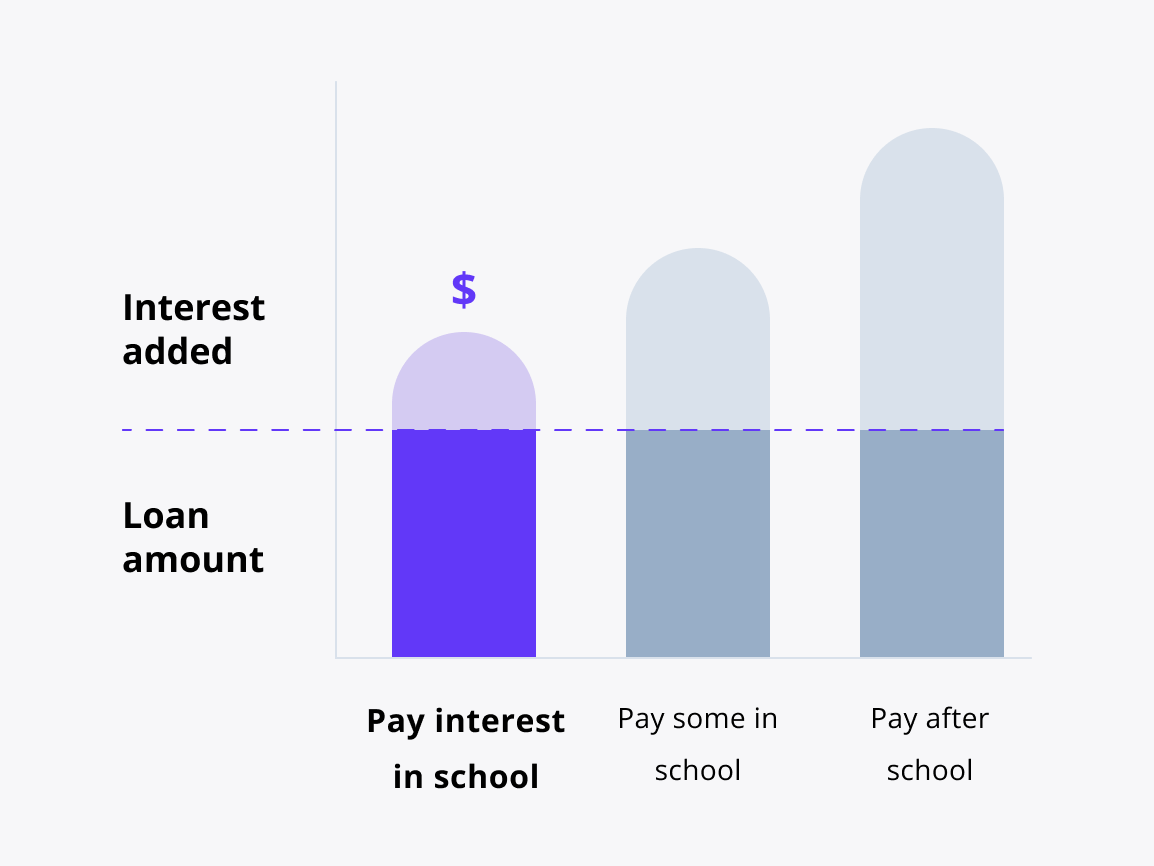

Interest repayment option

How does it work?

You pay your interest every month you’re in school and in grace (the 6 months after).footnote 1

This is a great option if you want to save the most on your total loan cost.

Keep in mind:

You might have higher monthly payments, but the total cost of your loan may be lower.

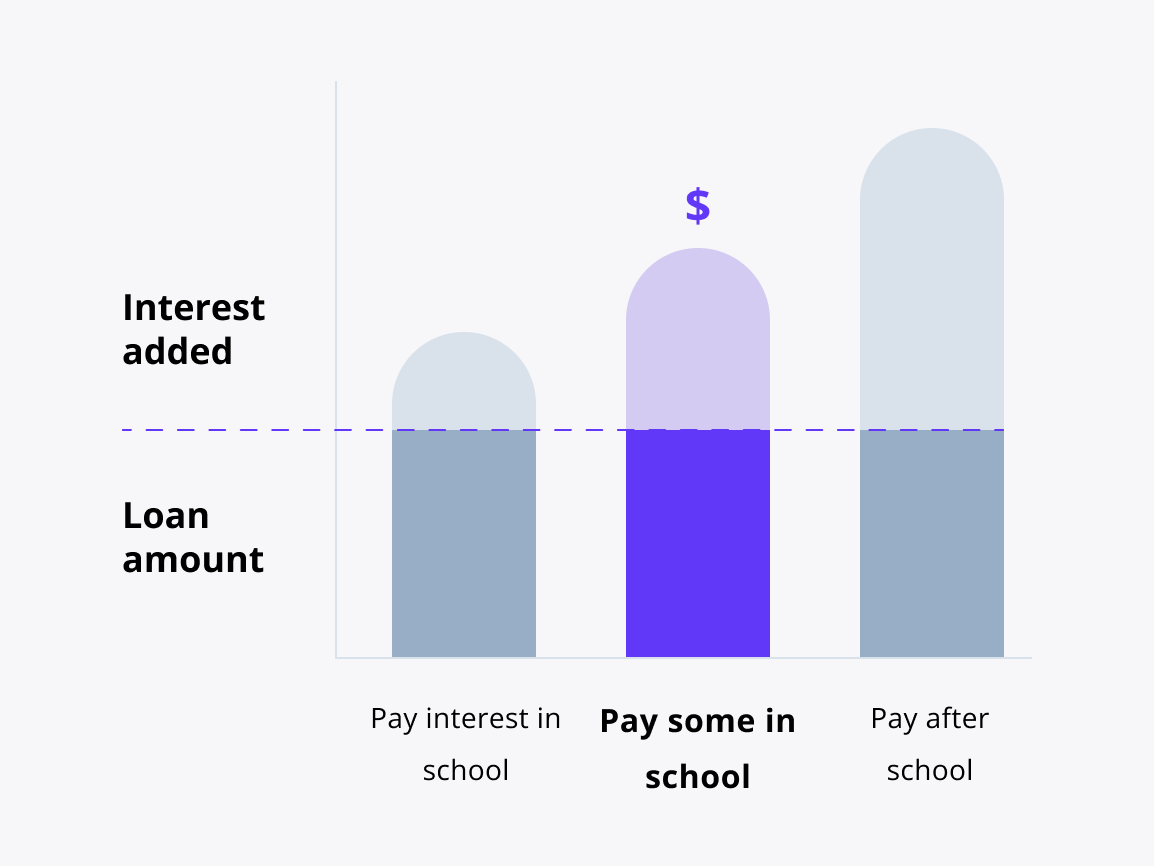

Fixed repayment option

How does it work?

You pay $25 every monthfootnote 6 you’re in school and in grace.footnote 1

This is a great option if you want to make a dent in payments from the start.

Keep in mind:

Any interest you don’t pay during school will be added to your principal amount (total borrowed) after grace.

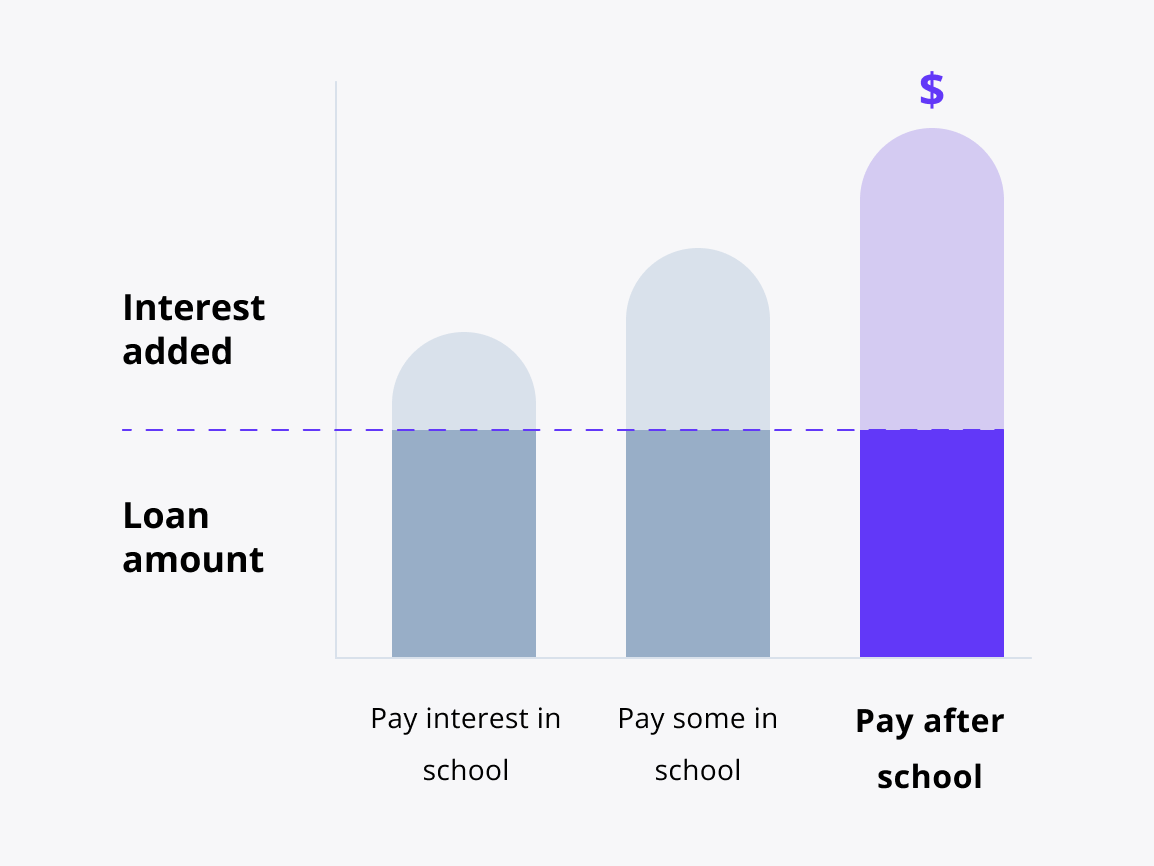

Deferred repayment option

How does it work?

You’ll have no scheduled payments while you’re in school and in grace.footnote 1

This is a great option if you want to focus on class and not on making loan payments.

Keep in mind:

The total cost of your loan may be higher because the interest you don’t pay on your loan while you’re in school and grace will be added to the original amount you borrowed (principal amount).

minutes

1. Tell us some basics

2. Choose your loan options

3. Sign and accept

Are you going for an advanced nursing degree?

Our graduate school loan for health professions can help you pay for a graduate-level health degree.

FAQs

Have other questions? We’re here to help.

1-877-279-7172

Do I need a cosigner?

Private student loans are credit-based, which means we check students’ credit when they apply. Last year, students were 4X more likely to be approved with a cosigner.footnote 4 A cosigner is an adult with good credit, usually a parent, who shares responsibility with you for paying back the undergraduate student loan.

Why should I borrow for the entire school year?

You can apply just once a year with a single credit check and funds are sent for each term directly to your school. You can cancel future disbursements as needed with no penalty. Interest isn't charged on funds until they are sent to your school, so you can relax, knowing you've got the funds when you need them.

How long does it take to get a Smart Option Student Loan?

It takes about 10 minutes to apply and get a credit decision. After you’re approved, you choose your loan rate type and repayment options, accept your loan disclosure, e-sign and provide any other requested information, and the loan is certified by your school. We send (disburse) the funds directly to the school. The process can take as few as 10 business days from application to disbursement.

Can I qualify if attending school online, or less than half-time?

Whether you study online or on campus, you can borrow to cover the costs at a participating institution, even if you're not a full- or half-time student. The loan's flexibility makes it a good choice for many situations:

- Attending school full-time, half-time, or less than half-time

- Online or on-campus classes

- Winter or summer classes

- Study abroad

- Professional certification courses

- A U.S. citizen or permanent resident enrolled in a school in a foreign country

- Students who are not U.S. citizens or permanent residents residing in and attending school in the U.S. (with a cosigner who is a U.S. citizen or U.S. permanent resident)

When do I start paying back my student loan?

With the Smart Option Student Loan, you can select from three repayment options. While in school, you can choose to make monthly interest payments or fixed $25 payments,footnote 6—or you can choose to defer payments until after school.footnote 1 The repayment option you choose applies during school and for six months after you leave school (your grace period). After that, you begin to make principal and interest payments.

How do you decide if I qualify for a student loan?

When you apply, we look at your history of borrowing money and paying it back on time. Lenders want to know how responsible you are with credit before approving your student loan application. Many college-bound high school students haven’t had time to build up their own credit. That’s why they apply with a cosigner, a creditworthy adult who shares the responsibility of the student loan.

What information do I need when applying with a cosigner?

You and your cosigner will want to have your school information, amount needed (remember, you can use it to pay for school-certified expenses for the entire year) as well as your cosigner’s financial and employment information. You or your cosigner may start the application, however, should your cosigner not be with you, we can send along an email with a link to their section of the application so they can fill it in later.