Finance your future with an MBA student loan

Pay for your business school expenses as you pursue your Master of Business Administration degree.

3.49%

to 14.48% APRfootnote 1

What are fixed rates?

Fixed means your interest rate never changes.

If you want a predictable monthly payment, this is the way to go.

4.54%

to 13.98% APRfootnote 1

What are variable rates?

Variable interest rates go up or down as the market changes.

This means your monthly payments may also change—they might be higher if interest rates rise and lower if they fall.

MBA student loan benefits

Up to 100% coverage

of your school-certified costs like tuition, fees, housing, meals, travel, and more.footnote 4

Graduate borrowers were 2x more likely to get approved without a cosigner than undergraduates last year.footnote 5

Make 12 interest-only payments after your grace period.footnote 6

Months of deferment during your residency and fellowship.footnote 7

Month grace period to support you during your business career.footnote 8

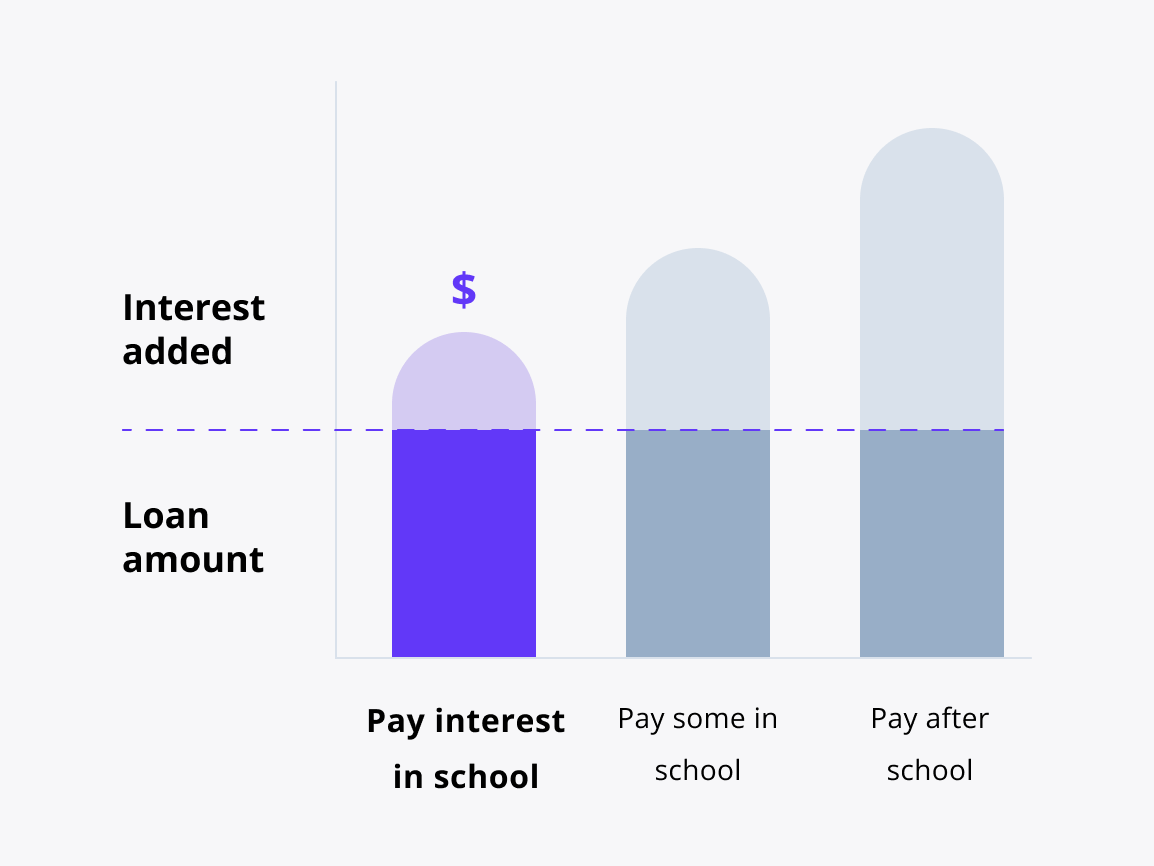

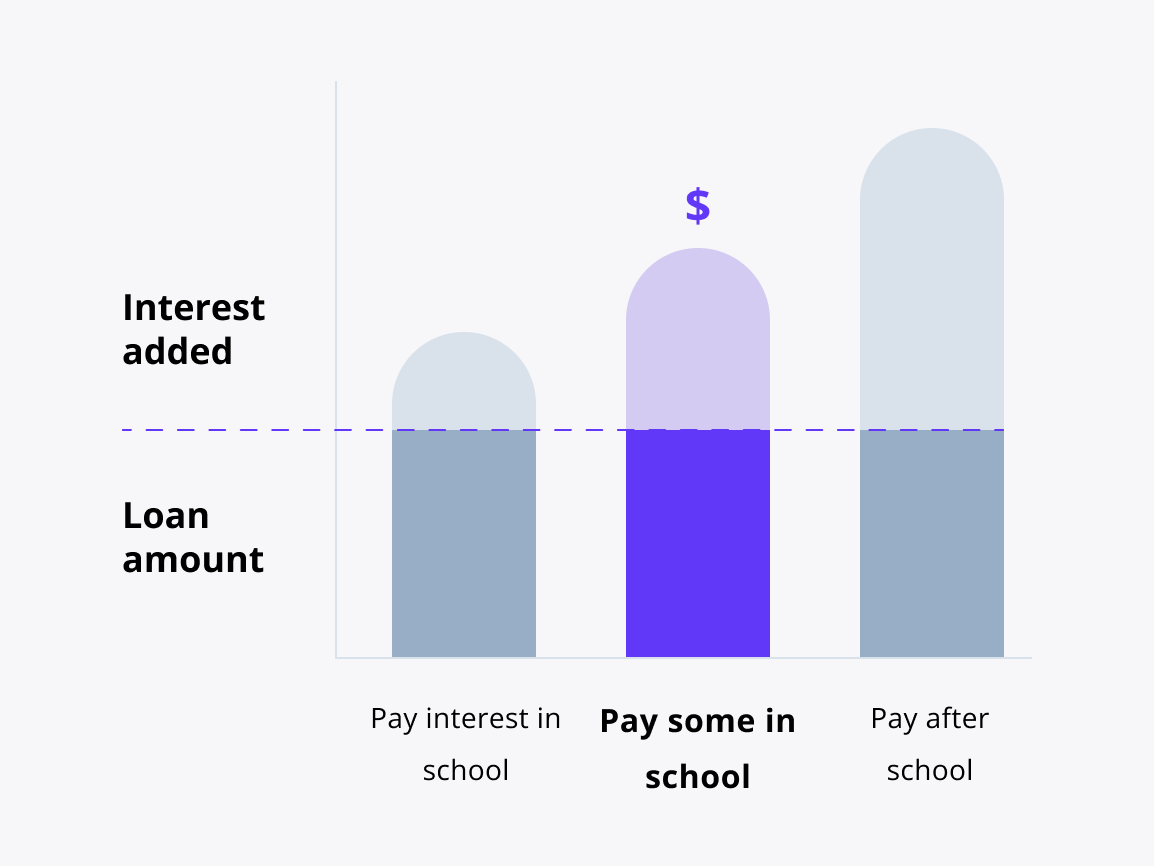

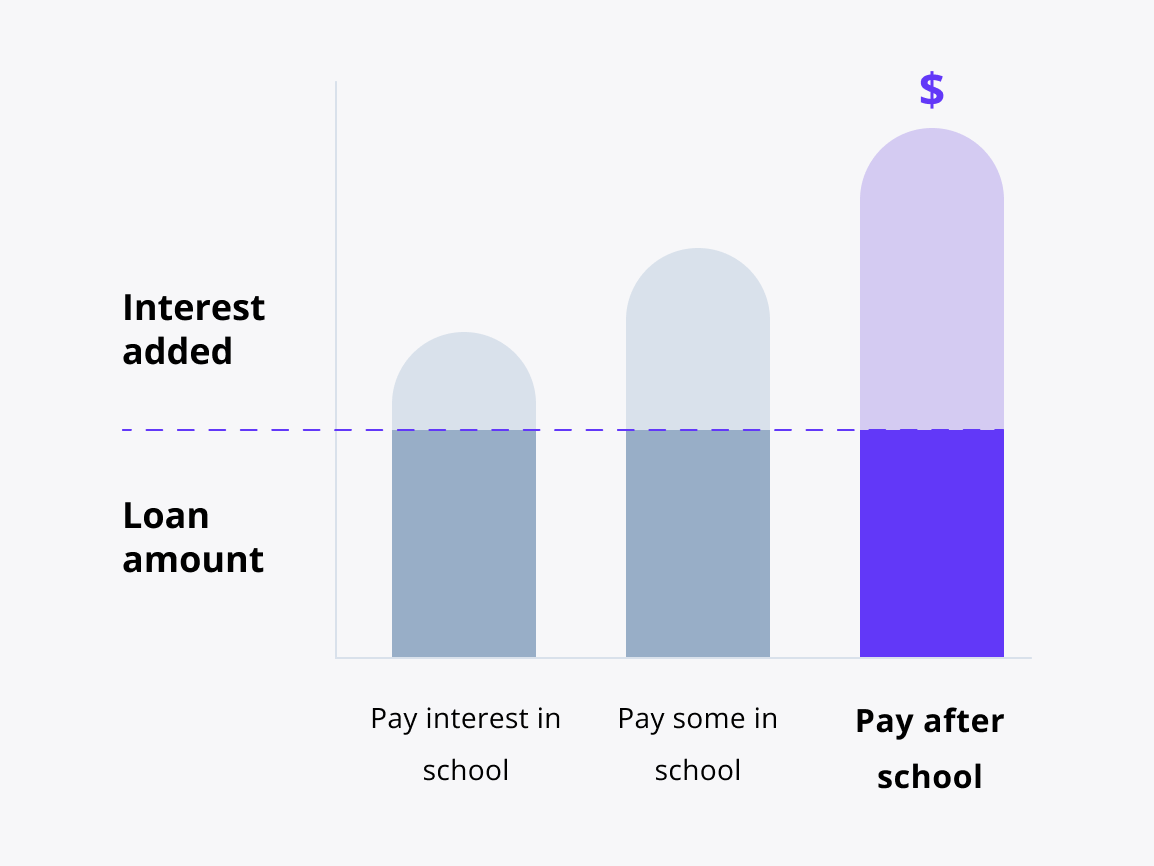

Breaking down your repayment options

Interest repayment option

How does it work?

You pay your interest every month you’re in school and in grace (the 6 months after).footnote 1

This is a great option if you want to save the most.

Students may get an interest rate that is .50 percentage points lower than deferred repayment.footnote 1

Keep in mind:

You might have higher monthly payments, but the total cost of your loan may be lower.

Fixed repayment option

How does it work?

You pay $25 every monthfootnote 9 you’re in school and in grace.footnote 1

This is a great option if you want to make a dent in payments from the start.

Students may get an interest rate that is .25 percentage points lower than deferred repayment.footnote 1

Keep in mind:

Any interest you don’t pay during school will be added to your principal amount (total borrowed) after grace.

Deferred repayment option

How does it work?

You’ll have no scheduled payments while you’re in school and in grace.footnote 1

This is a great option if you want to focus on class and not on making loan payments.

Keep in mind:

The total cost of your loan may be higher because the interest you don’t pay on your loan while you’re in school and grace will be added to the original amount you borrowed (principal amount).

What you gain with our MBA student loan

|

Sallie Mae® MBA Student Loan |

Other competitors |

|

|---|---|---|

|

Less than half-time enrollment eligibility |

|

|

|

Apply for cosigner release after 12 months of on-time principal and interest payments and credit requirements have been metfootnote 10 |

|

|

|

Interest-only payments for 12 months after grace period for qualifying graduate loan borrowersfootnote 6 |

|

|

|

Cover up to 100% of the cost of attendance minus financial aidfootnote 4 |

|

|

|

Fixed and variable interest rate options |

|

|

|

In-school or deferred repayment options for graduate loan borrowersfootnote 1 |

|

|

minutes

1. Tell us some basics

2. Choose your loan options

3. Sign and accept

Let's make sure you're ready

You'll need a few things to apply like address, Social Security number (if you have one), and details about your school.

FAQs

Have other questions? We’re here to help.

1-877-279-7172

What is an MBA loan?

An MBA loan is a loan to help pay for your business school expenses while getting your Master of Business Administration degree.

What does an MBA private student loan cover?

An MBA private student loan can be used to cover an entire school year’s expenses, including tuition, fees, books, housing, meals, travel, and technology.footnote 4 MBA loans cannot be used for personal expenses unrelated to education, like high-risk investments, debt repayment, or business startups.

If you receive more funds than you need, consider paying back your loan to get ahead of interest and principal payments.

What are the eligibility criteria for obtaining an MBA loan?

MBA Loans are for graduate students in an M.B.A. program at participating degree-granting schools and are subject to credit approval, identity verification, signed loan documents, and school certification. Student or cosigner must meet the age of majority in their state of residence. Students who are not U.S. citizens or U.S. permanent residents must reside in the U.S., attend school in the U.S., apply with a creditworthy cosigner (who must be a U.S. citizen or U.S. permanent resident), and provide an unexpired government-issued photo ID. Requested loan amount must be at least $1,000.

To fill out the application, you’ll need your personal information, including your full name, date of birth, Social Security number (if you have one), and contact details. You’ll also need to provide school details, including the name of the MBA program, enrollment status, and anticipated graduation date. Financial information needed includes income and any other relevant financial details.

What’s the maximum amount I can borrow with an MBA loan?

The loan amount cannot exceed the school-certified cost of attendance minus any financial aid received. The loan amount will be based on the total expenses associated with your business school education.

We encourage students to start with savings, grants, scholarships, and federal student loans to pay for college. You should also evaluate all anticipated monthly loan payments and how much you might earn in the future (if possible) before considering a private student loan.

Do MBA programs offer financial aid?

To receive financial aid for MBA programs, start by filling out the Free Application for Federal Student Aid (FAFSA®) to determine your eligibility for federal loans and grants. You should submit your FAFSA® as soon as it opens to maximize your aid options. You should also prioritize applying for scholarships

Can I apply for an MBA loan without a cosigner, and how does having a cosigner affect the loan terms?

While applying without a cosigner is possible, having one may positively impact your approval process, eligibility, and loan terms. Having a creditworthy cosigner may help you qualify for lower interest rates. The most credit-worthy applicants who choose the interest repayment option may receive the lowest rate.

Cosigners must meet specific criteria, including U.S. citizenship or permanent residency. A creditworthy cosigner may help you qualify for lower interest rates—and different repayment options can affect overall costs.